Learning to Price Homogeneous Data

Keran Chen ⋅ Joon Suk Huh ⋅ Kirthevasan Kandasamy

2024 Poster

{kind=link}

Abstract

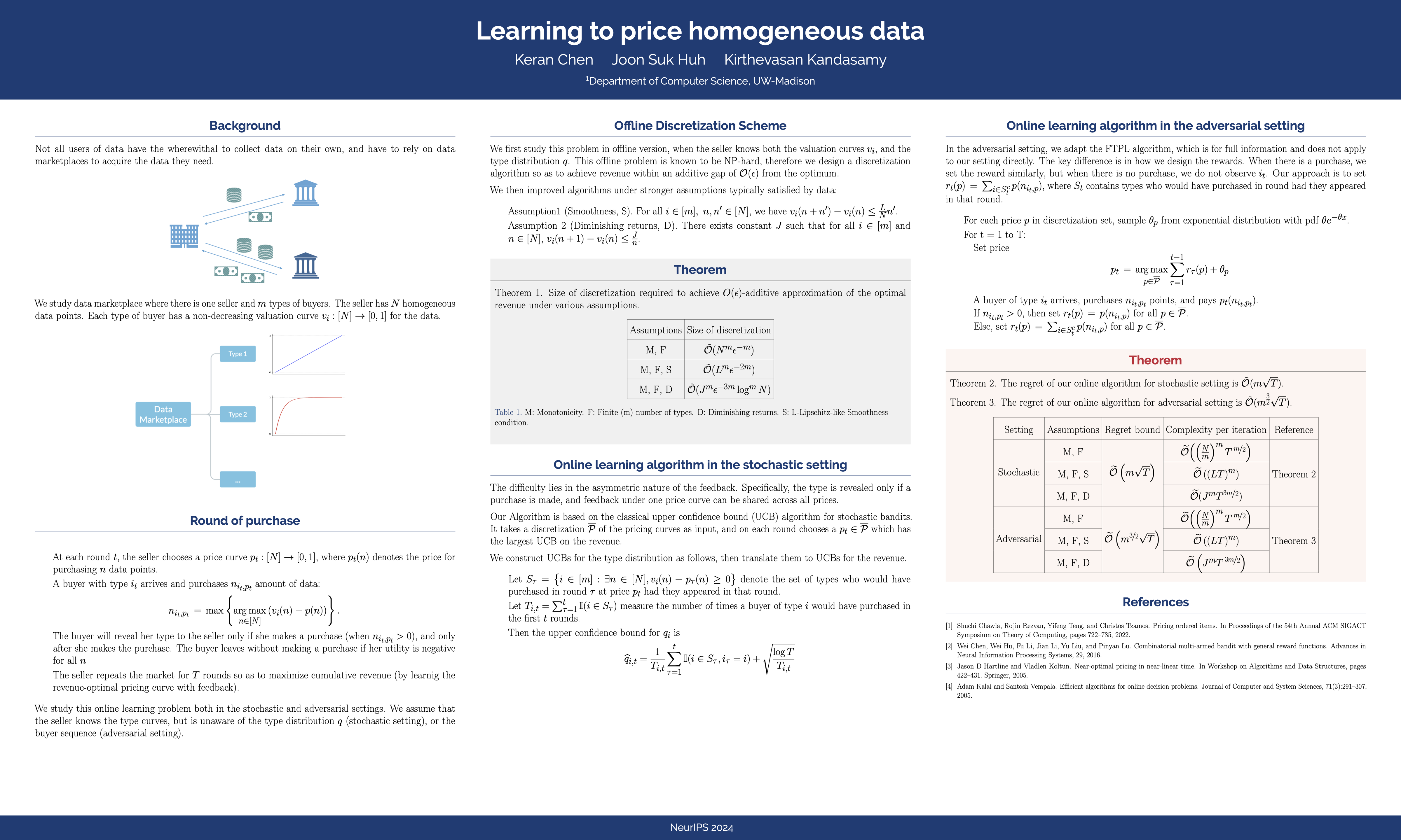

We study a data pricing problem, where a seller has access to $N$ homogeneous data points (e.g. drawn i.i.d. from some distribution).There are $m$ types of buyers in the market, where buyers of the same type $i$ have the same valuation curve $v_i:[N]\rightarrow [0,1]$, where $v_i(n)$ is the value for having $n$ data points.*A priori*, the seller is unaware of thedistribution of buyers, but can repeat the market for $T$ rounds so as to learn the revenue-optimal pricing curve $p:[N] \rightarrow [0, 1]$.To solve this online learning problem,we first develop novel discretization schemes to approximate any pricing curve.When compared to prior work,the size of our discretization schemes scales gracefully with the approximation parameter, which translates to better regret in online learning.Under assumptions like smoothness and diminishing returns which are satisfied by data, the discretization size can be reduced further.We then turn to the online learning problem, both in the stochastic and adversarial settings.On each round, the seller chooses an *anonymous* pricing curve $p_t$.A new buyer appears and may choose to purchase some amount of data.She then reveals her type *only if* she makes a purchase.Our online algorithms build on classical algorithms such as UCB and FTPL, but require novel ideas to account for the asymmetric nature of this feedback and to deal with the vastness of the space of pricing curves.Using the improved discretization schemes previously developed, we are able to achieve $\widetilde{O}(m\sqrt{T})$ regret in the stochastic setting and $\widetilde{\mathcal{O}}(m^{3/2}\sqrt{T})$ regret in the adversarial setting.

Video

Chat is not available.

Successful Page Load