Uncovering the short-time dynamics of electricity day-ahead markets

{kind=link}

Abstract

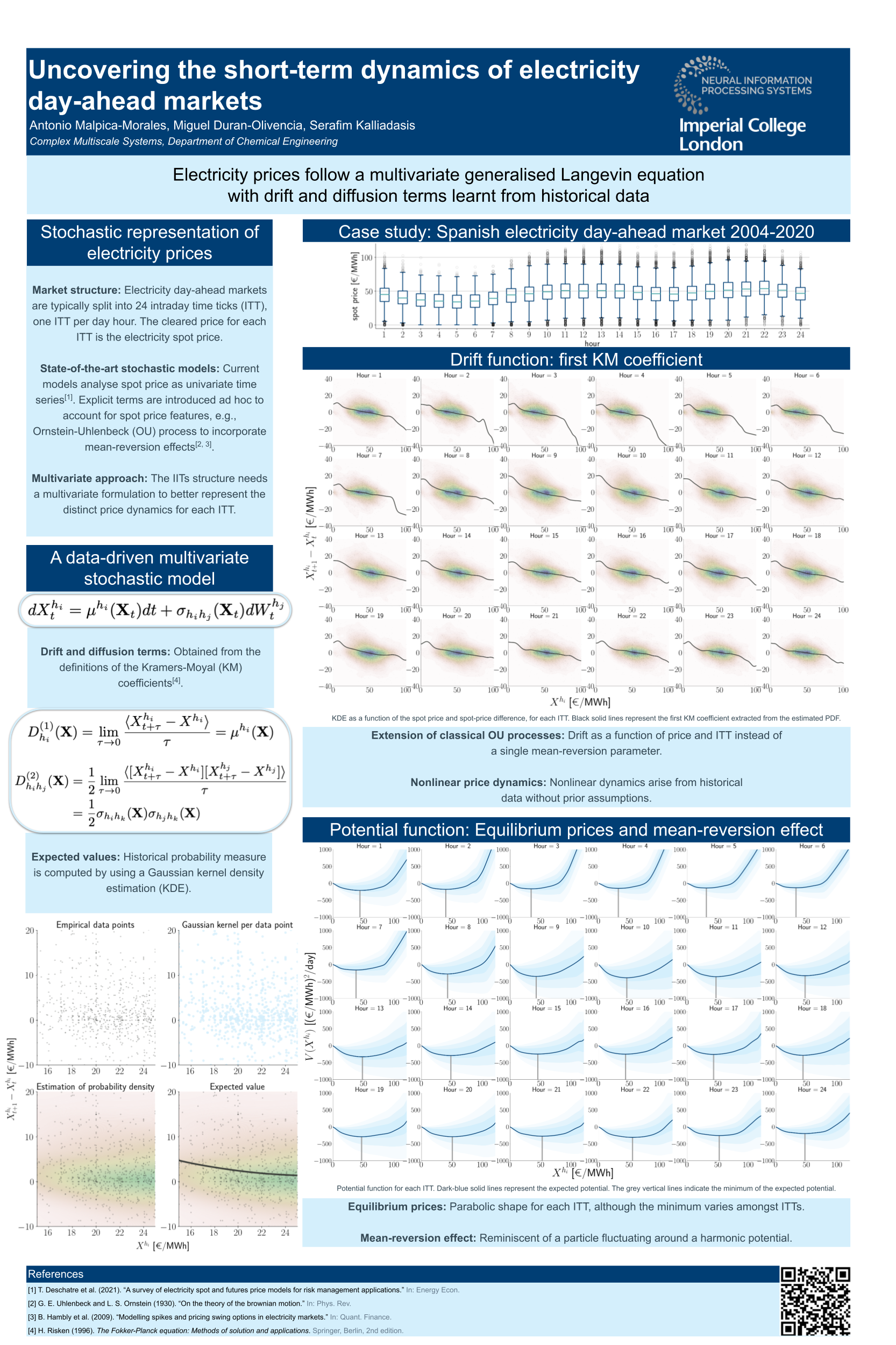

Obtaining a mathematical representation of electricity market prices is the cornerstone of the decision-making process in a liberalised landscape. Most of the existing models analyse the day-ahead electricity price as a univariate time series. This approach requires prior assumptions on the mathematical formulation to obtain an accurate representation of the time-evolution of electricity prices. We propose a new multivariate-stochastic-process model for the day-ahead prices, with each dimension of the process representing a single intraday time tick (ITT) auctioned in the day-ahead market. In this model, the electricity price at each ITT is the solution of a stochastic differential equation (so-called general Langevin equation) with the drift and diffusion terms to be learnt from historical data. The terms governing the stochastic differential equation are obtained by a kernel density estimation of the historical probability, to compute the expected values involved in the Kramers-Moyal definitions. The model is tested using data of the Spanish electricity day-ahead market, yielding a reliable representation of the electricity price structure.The price structure reveals the main features commonly discussed in electricity markets, such as the mean-reversion or equilibrium prices. Our results help us to understand the underlying short-time dynamics that govern the electricity day-ahead markets.