RAPTOR: Reasoned Agentic Portfolio Trading with Orchestrated Rebalancing

in

Workshop: NORA: The First Workshop on Knowledge Graphs & Agentic Systems Interplay

{kind=link}

Abstract

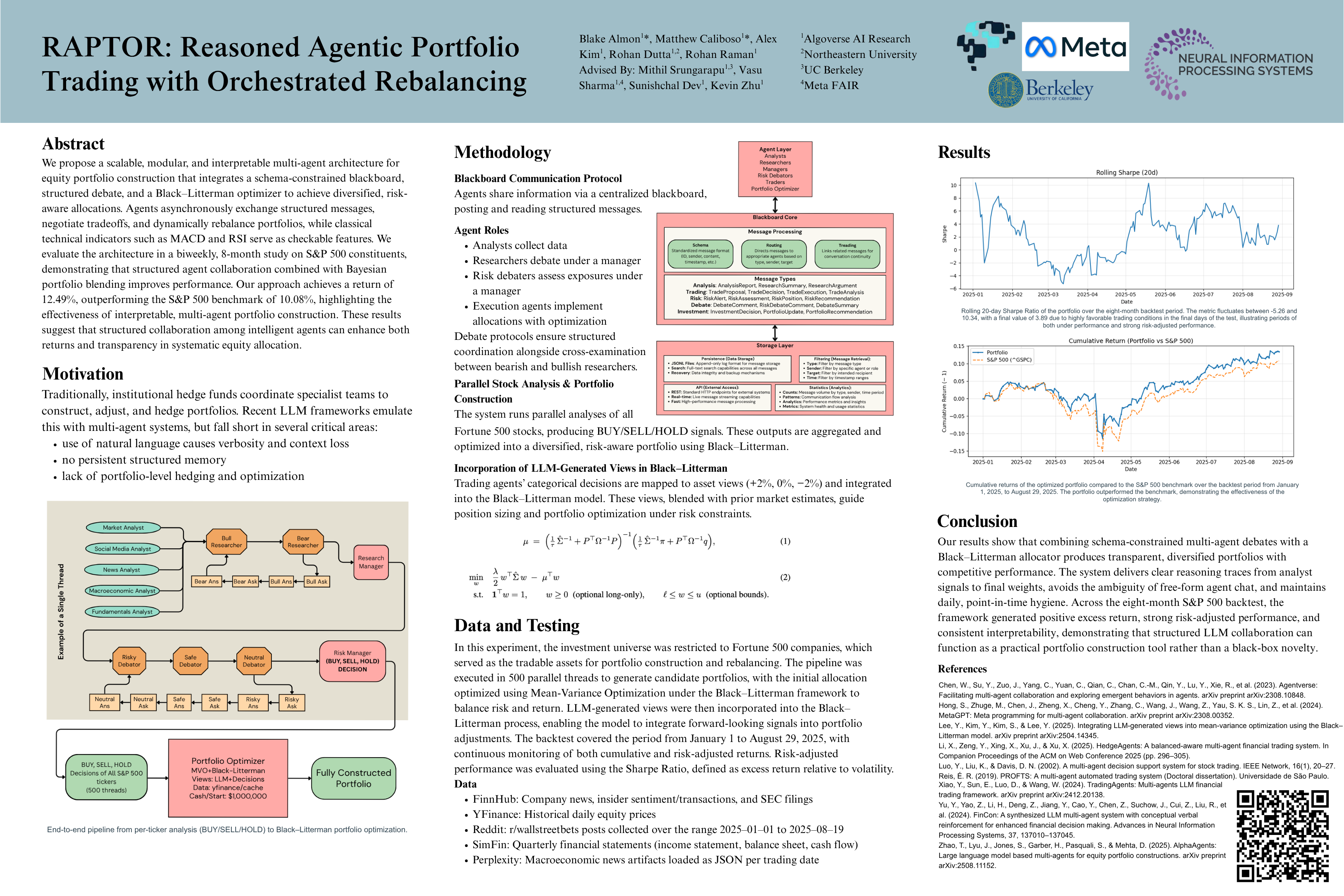

We propose an institutional-style, multi-agent architecture for equity portfolio construction that couples a schema-constrained blackboard with structured debate and a Black-Litterman optimizer, enabling diversified, risk-aware allocations. The system is scalable, modular, and interpretable, allowing agents to asynchronously exchange structured messages, negotiate tradeoffs, and dynamically rebalance portfolios. We analyze the performance of our approach in a biweekly, one-year reconstruction study on S&P 500 constituents, demonstrating that this combination of structured agent collaboration and Bayesian portfolio blending is practical and modular. We also operationalize a Chain-of-Alpha methodology, and allow classical indicators, for example, Moving Average Convergence Divergence (MACD) and Relative Strength Index (RSI) to serve as checkable features within each chain. Our approach achieves a return of 13.43% over the 8 month backtest, exceeding the S&P 500's 10.08% over the same time frame. The source code and data sets used are available anonymously at https://anonymous.4open.science/r/RAPTOR-Reasoned-Agentic-Portfolio-Trading-with-Orchestrated-Rebalancing