FinRL-Meta: Market Environments and Benchmarks for Data-Driven Financial Reinforcement Learning

{kind=link}

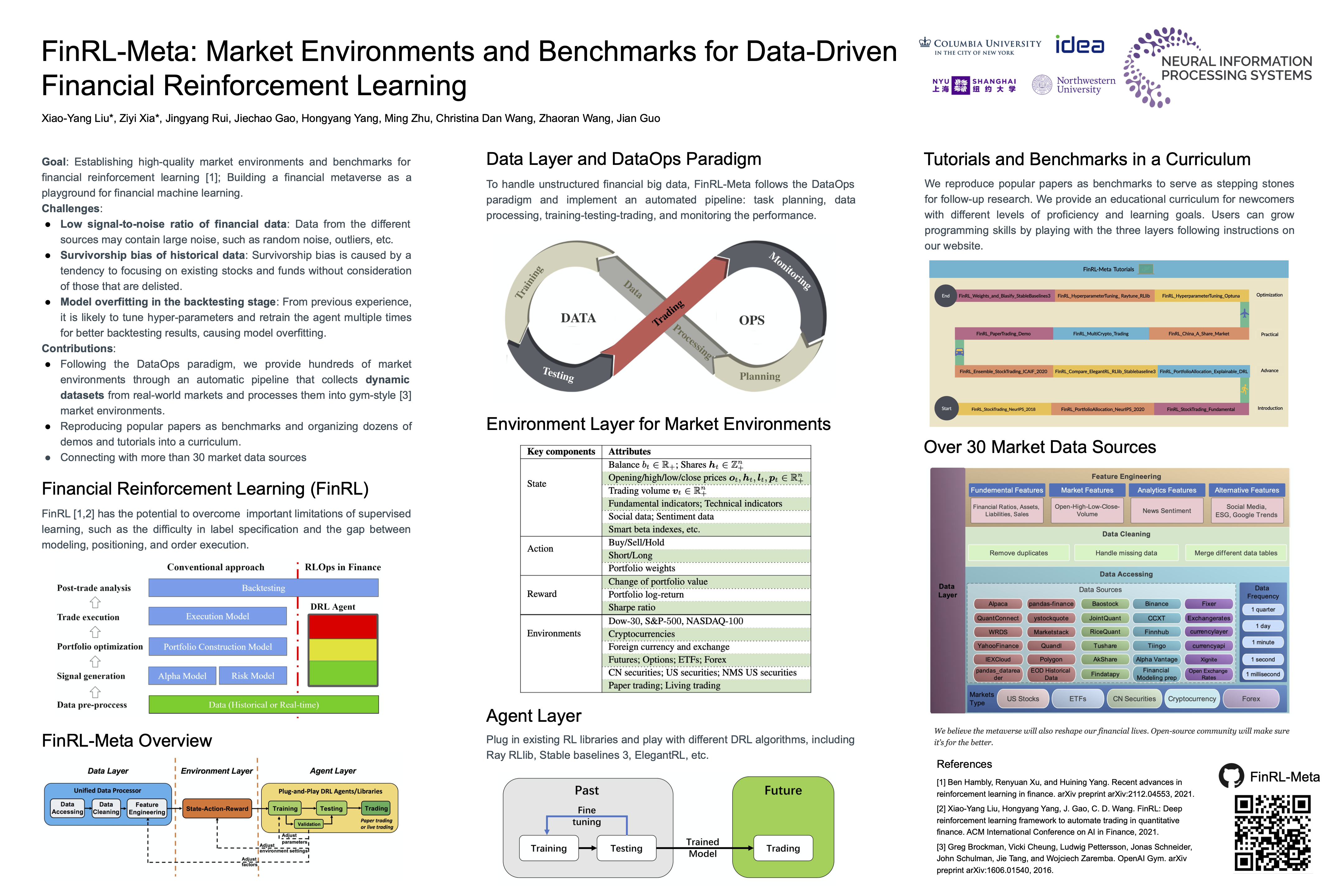

Abstract

Finance is a particularly challenging playground for deep reinforcement learning. However, establishing high-quality market environments and benchmarks for financial reinforcement learning is challenging due to three major factors, namely, low signal-to-noise ratio of financial data, survivorship bias of historical data, and backtesting overfitting. In this paper, we present an openly accessible FinRL-Meta library that has been actively maintained by the AI4Finance community. First, following a DataOps paradigm, we will provide hundreds of market environments through an automatic data curation pipeline that processes dynamic datasets from real-world markets into gym-style market environments. Second, we reproduce popular papers as stepping stones for users to design new trading strategies. We also deploy the library on cloud platforms so that users can visualize their own results and assess the relative performance via community-wise competitions. Third, FinRL-Meta provides tens of Jupyter/Python demos organized into a curriculum and a documentation website to serve the rapidly growing community. FinRL-Meta is available at: \url{https://github.com/AI4Finance-Foundation/FinRL-Meta}