Data-Dependent Bounds for Online Portfolio Selection Without Lipschitzness and Smoothness

Chung-En Tsai ⋅ Ying-Ting Lin ⋅ Yen-Huan Li

2023 Poster

{kind=link}

Abstract

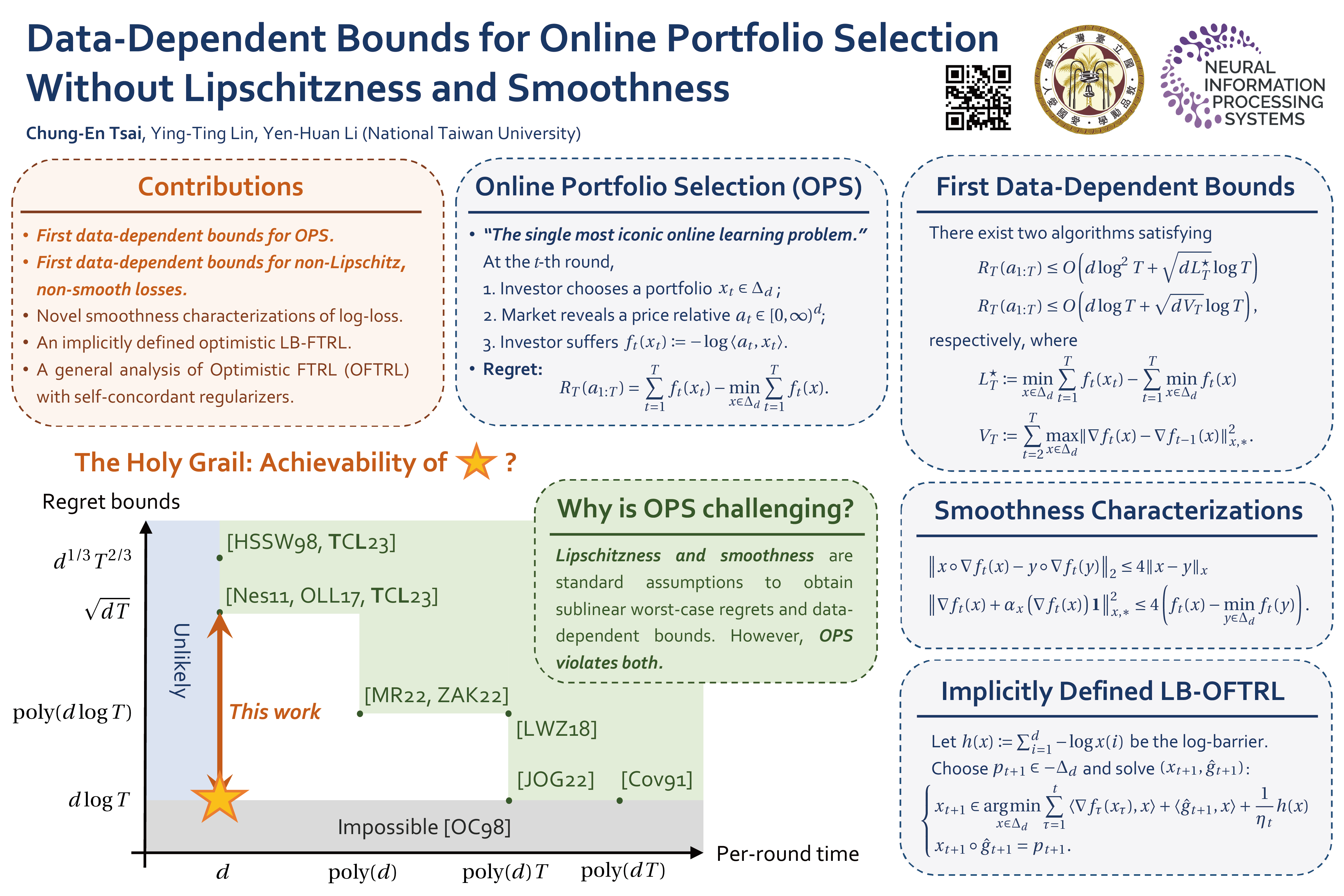

This work introduces the first small-loss and gradual-variation regret bounds for online portfolio selection, marking the first instances of data-dependent bounds for online convex optimization with non-Lipschitz, non-smooth losses. The algorithms we propose exhibit sublinear regret rates in the worst cases and achieve logarithmic regrets when the data is "easy," with per-round time almost linear in the number of investment alternatives. The regret bounds are derived using novel smoothness characterizations of the logarithmic loss, a local norm-based analysis of following the regularized leader (FTRL) with self-concordant regularizers, which are not necessarily barriers, and an implicit variant of optimistic FTRL with the log-barrier.

Video

Chat is not available.

Successful Page Load