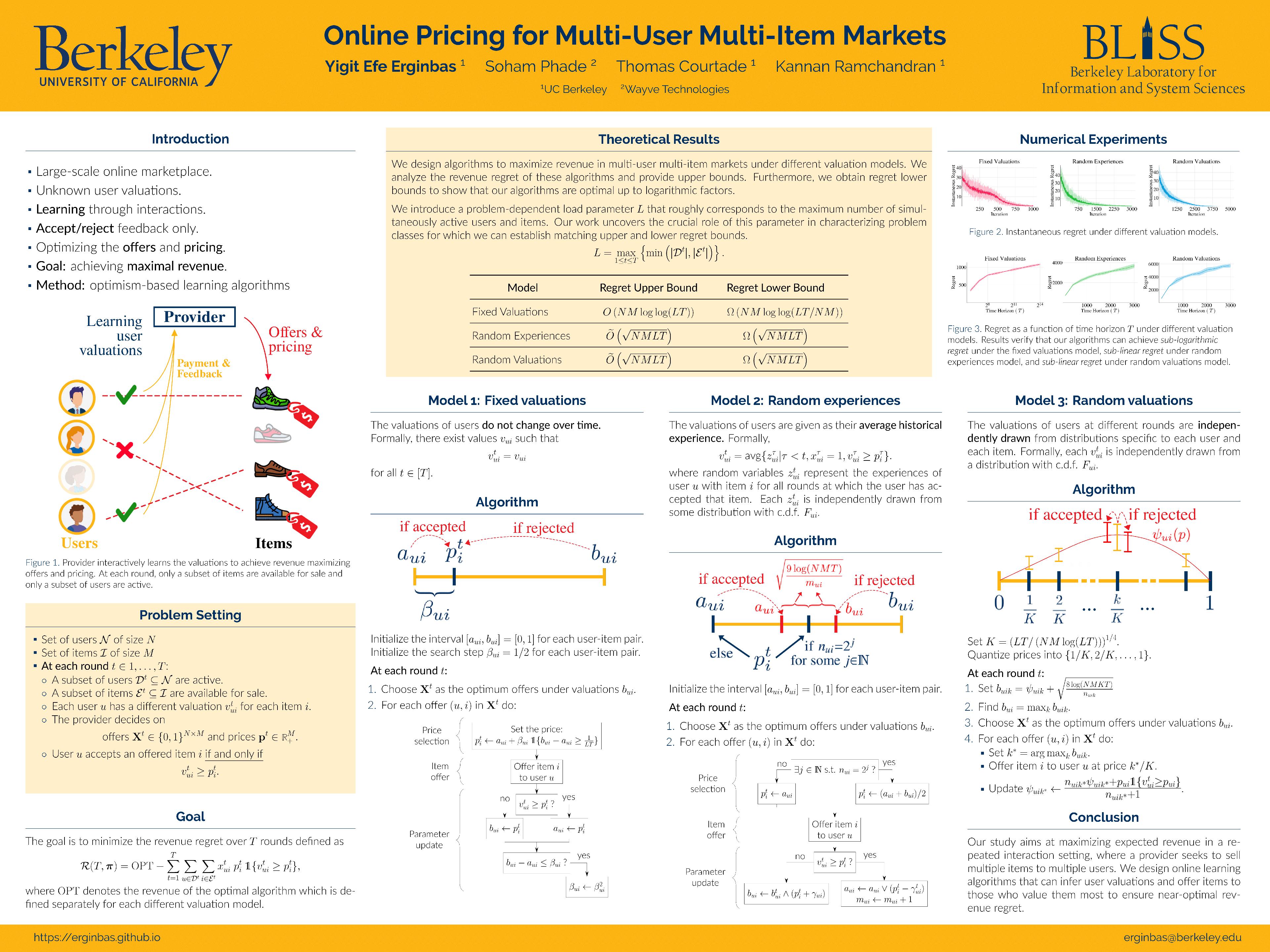

Online Pricing for Multi-User Multi-Item Markets

Yigit Efe Erginbas ⋅ Thomas Courtade ⋅ Kannan Ramchandran ⋅ Soham Phade

2023 Poster

{kind=link}

Abstract

Online pricing has been the focus of extensive research in recent years, particularly in the context of selling an item to sequentially arriving users. However, what if a provider wants to maximize revenue by selling multiple items to multiple users in each round? This presents a complex problem, as the provider must intelligently offer the items to those users who value them the most without exceeding their highest acceptable prices. In this study, we tackle this challenge by designing online algorithms that can efficiently offer and price items while learning user valuations from accept/reject feedback. We focus on three user valuation models (fixed valuations, random experiences, and random valuations) and provide algorithms with nearly-optimal revenue regret guarantees. In particular, for any market setting with $N$ users, $M$ items, and load $L$ (which roughly corresponds to the maximum number of simultaneous allocations possible), our algorithms achieve regret of order $O(NM\log\log(LT))$ under fixed valuations model, $\widetilde{O}(\sqrt{NMLT})$ under random experiences model and $\widetilde{O}(\sqrt{NMLT})$ under random valuations model in $T$ rounds.

Video

Chat is not available.

Successful Page Load