Debiasing Conditional Stochastic Optimization

{kind=link}

Abstract

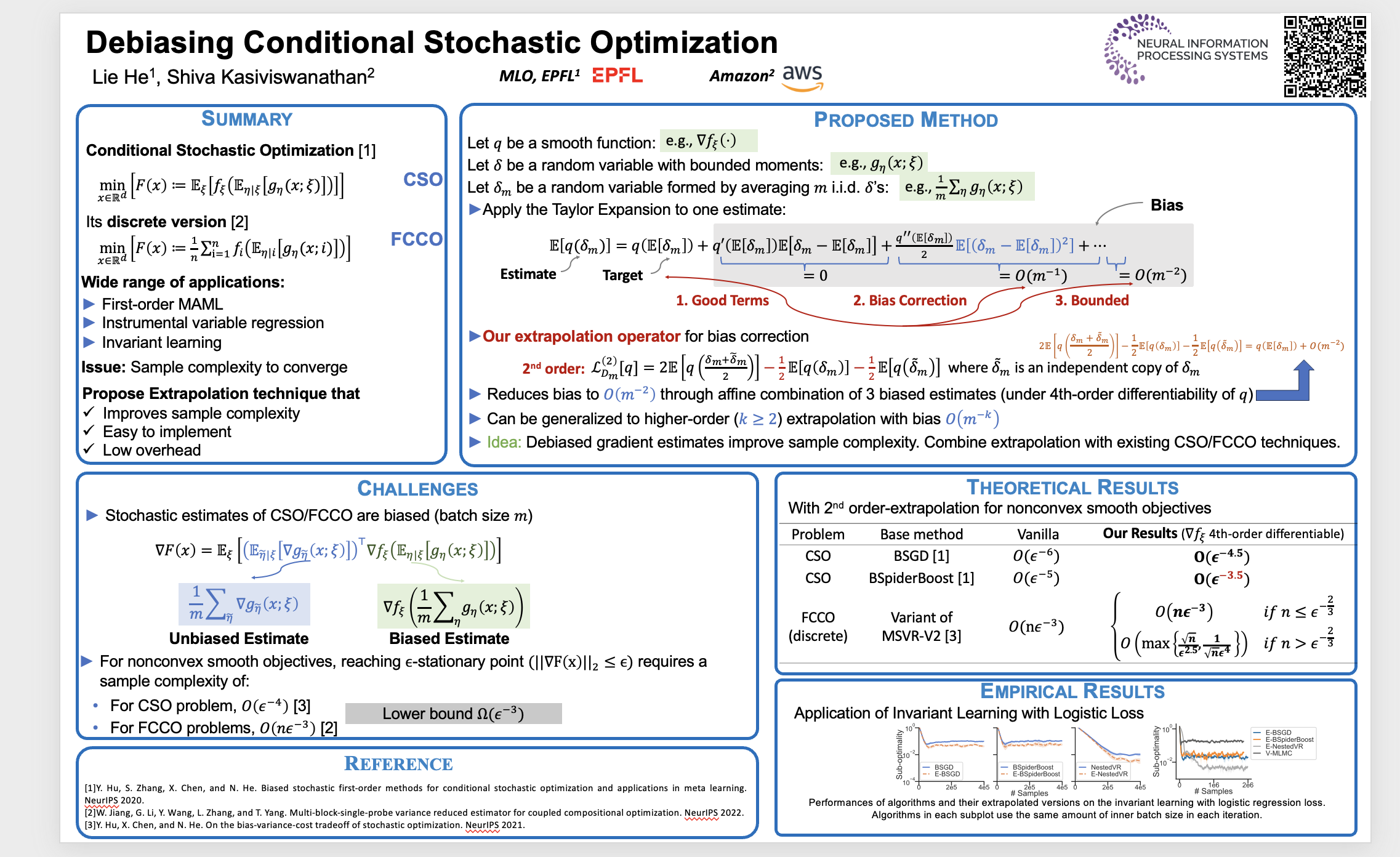

In this paper, we study the conditional stochastic optimization (CSO) problem which covers a variety of applications including portfolio selection, reinforcement learning, robust learning, causal inference, etc. The sample-averaged gradient of the CSO objective is biased due to its nested structure, and therefore requires a high sample complexity for convergence. We introduce a general stochastic extrapolation technique that effectively reduces the bias. We show that for nonconvex smooth objectives, combining this extrapolation with variance reduction techniques can achieve a significantly better sample complexity than the existing bounds. Additionally, we develop new algorithms for the finite-sum variant of the CSO problem that also significantly improve upon existing results. Finally, we believe that our debiasing technique has the potential to be a useful tool for addressing similar challenges in other stochastic optimization problems.