Exploring Modern Evolution Strategies in Portfolio Optimization

{kind=link}

Abstract

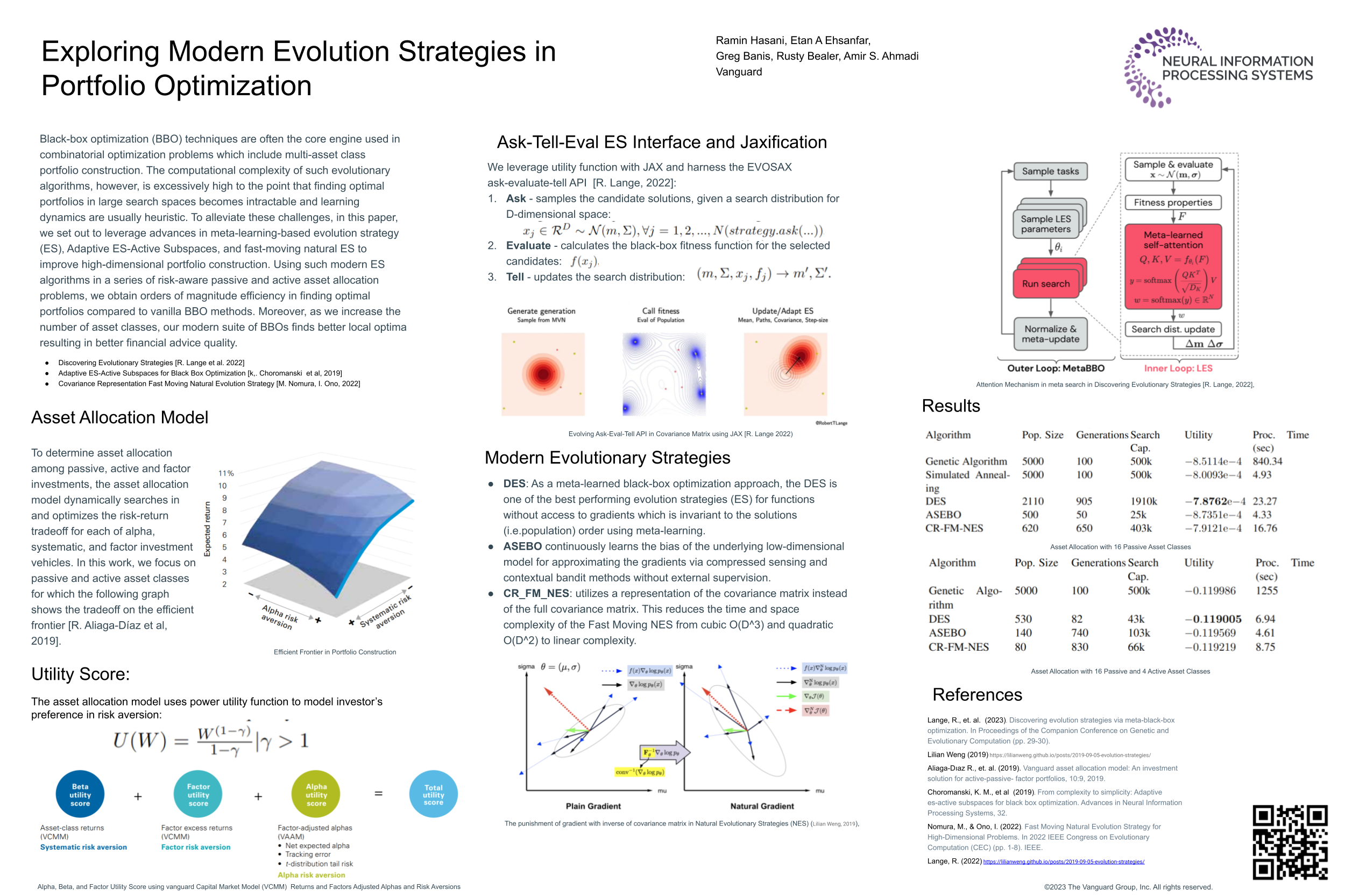

Black-box optimization (BBO) techniques are often the core engine used in combinatorial optimization problems which include multi-asset class portfolio construction. The computational complexity of such evolutionary algorithms, however, is excessively high to the point that finding optimal portfolios in large search spaces becomes intractable. Additionally, the learning dynamics of BBO methods are typically heuristic as they do not use gradient evolutions. To alleviate these challenges, in this paper, we set out to leverage advances in meta-learning-based evolution strategy (ES), Adaptive ES-Active Subspaces, and fast-moving natural ES to improve high-dimensional and large search space portfolio optimization. Using such modern ES algorithms in a series of risk-aware passive and active asset allocation problems, we obtain one to three orders of magnitude efficiency in finding optimal portfolios compared to vanilla BBO methods. Moreover, as we increase the number of asset classes, our modern suite of BBOs finds better local optima resulting in better financial advice quality.